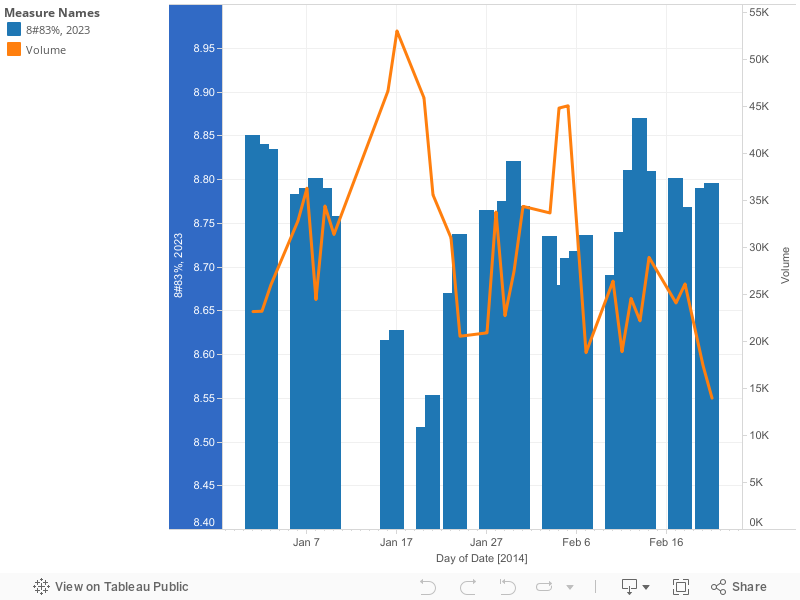

G-Sec markets have become extremely sideways in the last one month - starting with the release of Urjit Patel Committee's report. The following chart highlights the same:

Since the beginning of February (despite the Fab start to February), the 10Y bond has been mostly trading in the 8.70-8.80 zone with declining volumes despite the flurry of good news (in CPI & WPI) and slightly incredible news (like the Vote on Account).

Since the beginning of February (despite the Fab start to February), the 10Y bond has been mostly trading in the 8.70-8.80 zone with declining volumes despite the flurry of good news (in CPI & WPI) and slightly incredible news (like the Vote on Account).

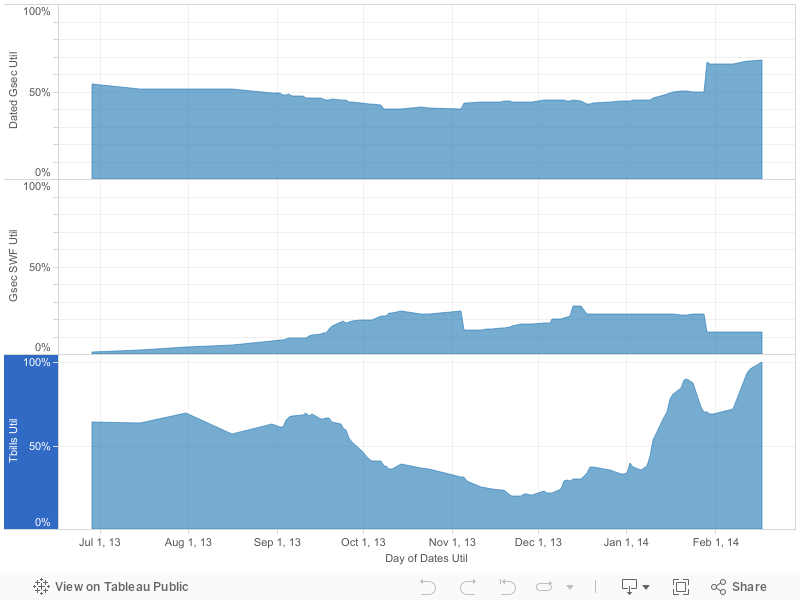

At this point, it is interesting to note the below chart on FII debt utilization status:

Three points to ponder:

At this point, it is interesting to note the below chart on FII debt utilization status:

Three points to ponder:

- FIIs have fully utilized their T-bill quota. This broadly means they cannot bring in money to invest in T-bills when the Tbill issuance is higher than in January and perceived tightness in March. This supply-demand mismatch in short end of the yield curve is likely to keep the short term yields high - close to the MSF rate.

- For domestic investors, with no rate cut in sight, there is immense sense to invest in short end of the yield curve especially when it is inverted. The DIIs should continue to shift away from duration securities to short end of the curve.

- The above two points only suggests that the long term yields are sticky and I find them to be floored at 8.65-8.70 as we gradually move towards the next fiscal calendar.

At this point, as I suggested in my earlier post, the trading range for 10Y bond seems to be 8.65-8.80 for some more time.

No comments:

Post a Comment